For years, analysts have gone on channels like CNBC calling Bitcoin “digital gold”, and many everyday crypto investors truly believe that. But gold has been a “store of value” for millennia. Could Bitcoin, as we know it today, retain its value long term, say even just fifty years? The simple math tells us it likely can’t. Lets dig into why.

Bitcoin (as we know it) faces a major issue in the coming decades: its miner rewards are vanishing — essentially going to zero. This is because (written into its code) the number of bitcoins that miners receive per block mined drops by 50% every 4 years, aka the “halving”. (Put another way, well over 19.5M of the 21M bitcoins that will ever be mined have already been mined because of this. Investors gleefully scream: “scarcity!”, but I think they miss the forest for the trees.) Bitcoin miners are also rewarded via transaction fees but not even remotely to the extent that they are from mining’s base rewards. On average only about 3% of miner revenue comes from transaction fees, though on very rare (record setting) volume days, transaction fees can account for more than miner rewards[1].

A basic primer: Miners have to spend big to secure the Bitcoin network. It costs them a lot of money in electricity bills to “mine” new blocks. If mining profits drop, fewer miners will mine and -if enough drop out- the network’s difficulty rate will decline to the point that the network is no longer secure. For this very reason, many “small cap” coins suffer “51% attacks” [Many examples: 1,2,3,4,5]. They’re called “51% attacks” because it’s “an attack on the blockchain, where a group controls more than 50% of the hashing power”. In other words: any attacker who can spend more on electricity and compute hardware than the “good” miners will overwhelm and compromise the network. These attacks are devastating and usually mean a cryptocurrency is doomed. So maintaining sufficient miner rewards is… everything, in a “proof of work” system like Bitcoin’s.

A simple known truth: Twenty years from now, miners will make exactly 3.125% what they do today from base rewards per mined block. 40 years from now, that percentage drops to 0.09765625%. But miner profits are what keep the network secure, so, how will this turn out? Let’s dig further:

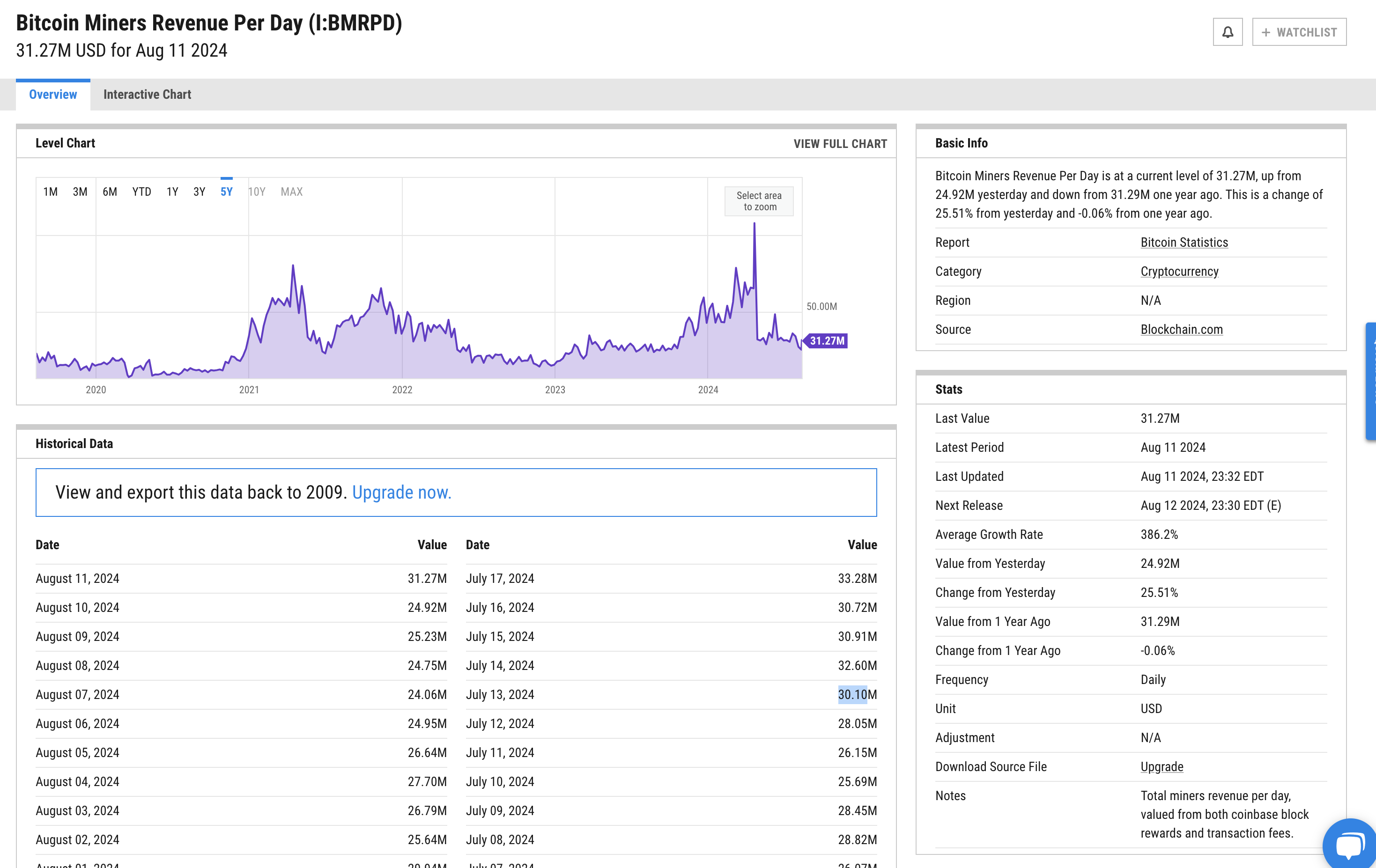

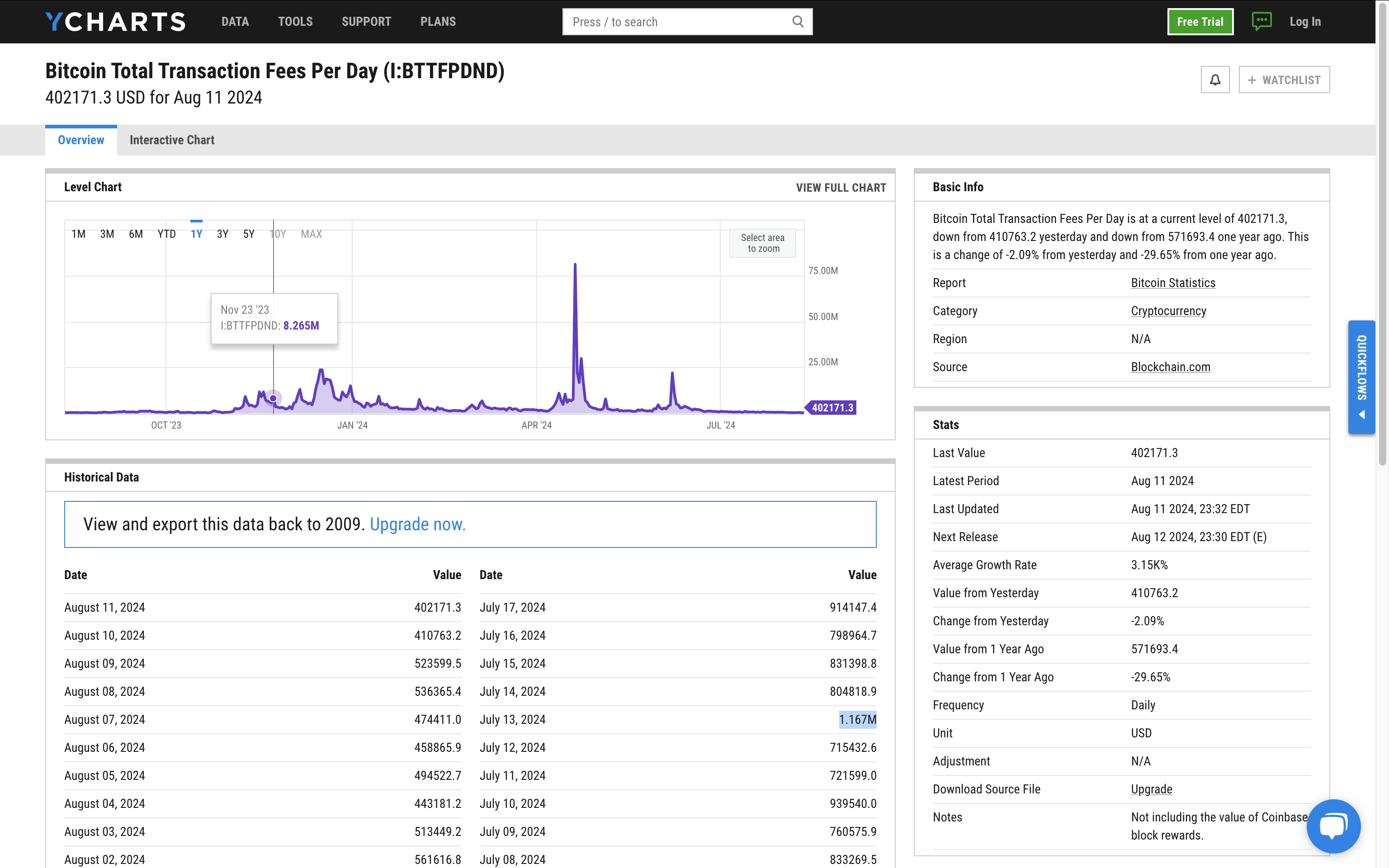

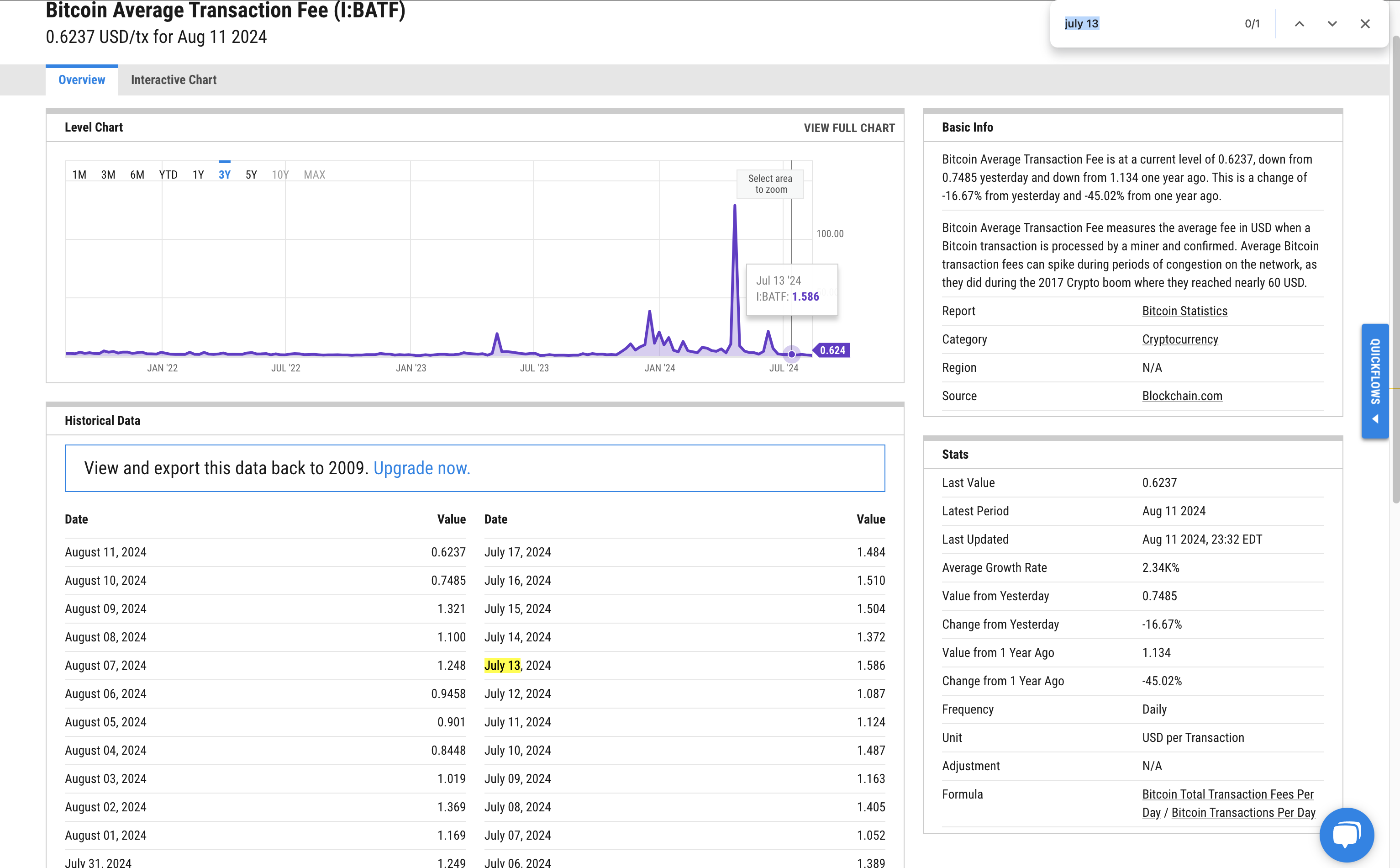

According to YCharts, on July 13th 2024, miners made a total of $30.1M USD worth of crypto for their work in securing the network and processing transactions. I chose July 13th because it was a fairly average day for Bitcoin. $30.1M is actually not that much money. (I can imagine plenty of nation-backed attackers who might be willing to spend far more than $30M per day to kill Bitcoin. 🤷♂️) But, for the purposes of this article, lets say that $30M+ is enough to secure the network. Of that ~$30.1M on July 13, only $1.167M was from transaction fees, or 3.89%. The fees per transaction on that day were fairly average if you look at a 3 year view, about $1.5 per transaction. And I’ll say I’m being charitable: that day’s $1.167M in transaction revenue was well over what it has been on average for the past month. (August 11th for example had $402K in transaction revenue on $31.27M in total revenue, so 1.3% of total miner revenue. But again, let’s be charitable and go with the July 13th numbers and 3.89%.)

{kind=link}

{kind=link}

{kind=link}

So, let’s say miners need to make ~$30M/day to defend against 51% attacks over the coming decades. There are precisely four ways that miners could theoretically continue to make roughly this amount of Bitcoin per day, but none of them reflect Bitcoin “as we know it”. 1) The price of Bitcoin continues to rise, to offset the “halvings”. 2 & 3) Transaction fees make up for the loss of base rewards, either by a.) jumping ~26x to ~$37.50 ($30.1 / $1.167 from the charitable numbers above) AND the volume of transactions somehow does not go down when that happens AND the volume of transactions is not volatile or b.) the volume of transactions goes up by ~26x , or 4) Bitcoin’s incentive structure, in its code, changes to not be deflationary.

Implausible Scenario #1: The price of Bitcoin continues to rise enough to offset its every-four-year “halving”. In order for that to happen, it would need to double in value every four years, which would double its market cap every four years too. Right now, Bitcoin has a value of about $60K and a market cap of about $1.1T. So, in 20 years, it would need to have a market cap of $35.2T to offset the “halving” effect. In 40 years, $1,126T, or $1.126 quadrillion, which is more than 10 times all the money in the world combined. Just for its base miner rewards to pay out $30M/day. Reaching a market cap higher than that is too ludicrous to consider. So basically, we can definitively say that, within 40 years, it’s impossible for Bitcoin’s possible rise in value to offset the “halving” effect.

Implausible Scenario #2: As we know: base rewards will decrease by ~97% over the next 20 years, so this scenario involves transaction fees making up for that by jumping by ~26x AND somehow not seeing the volume of transactions going down by a commensurate amount. This could theoretically make up for the revenue shortfall from decreased miner rewards. But this scenario seems extremely unlikely. In this scenario, instead of Bitcoin holders paying $1.5 on average to move their coin, they would need to pay ~$37.50 to move them, which would likely cause them to make fewer transactions, which reduces overall miner revenue. Currency is only useful if you can move it easily, or transfer it between people. In the early days of Bitcoin, people would talk about using Bitcoin to buy pizza or a cup of coffee. Can you imagine if Visa had a $37.50 charge per transaction? Businesses already gripe about the ~2% that credit cards take. This increase in transaction fees would be necessary to pay the miners, but also spell doom for Bitcoin as a useful currency. There’s this thing called the Lightning Network project, which addresses transaction speeds for end users, but does nothing to directly address miners’ impending revenue shortfall.

So the first issue with scenario #2 is somehow having $37.50 avg transaction fees without killing transaction volume. But the SECOND issue is even thornier: the historical volatility of transaction volume. If you look at the chart of daily transaction fee revenue, you can see that on some days, relatively few transactions happen, while on other days a ton of transactions happen. Whereas miner rewards are perfectly consistent and predictable, transaction volume is anything but. So lets say if, 20 years from now, transaction fees somehow make up for the 97%+ decrease in miner rewards, what happens on a day with far fewer transactions? Miners would have less incentive to mine, and a 51% attack would be cheap.

Implausible Scenario #3: Okay, but what if Bitcoin’s usage (transaction volume) went up by 26x, thus making up for the revenue in this way? However unlikely, this is the only real way to get through the implausible scenarios. The bitcoin network itself isn’t built to handle a lot of transactions (its blockchain size is already super large and inefficient). But, theoretically, something like the Lightning Network (if tons of people adopt it), could lead to a ton more transactions. A few issues with that particular route: a.) I’ve found Lightning Network’s approach rather clunky (you have to transfer BTC into a Lightning node, which adds a step I’m not sure many would take). b.) It advertises “exceptionally low fees”, which kind of defeats any chance of charging people enough money per transaction to make up for the revenue shortfall. c.) It’s been live for about a year, and there are no outward-facing signs (that I know of) that it is seeing massive adoption.

And then, finally, even if transaction volume went up by 26x, via Lightning or some other project, Bitcoin’s complete reliance on transaction fees would still leave it saddled with the volatility issue (where a prolonged lull in transactions would leave the network vulnerable).

Plausible Scenario #4: Eventually acknowledging this issue, the Bitcoin core developers change the project’s code to produce a fixed rate of base rewards per block, instead of a diminishing rate (much like Ethereum does (or did before the switch to proof of stake)), or move to proof of stake or something else.

Conclusion: Scenario #4 could fix the issue. It would also mean all the big Bitcoin advocates that have talked up the “there will never be more than 21M bitcoins” aspect of the coin to retail investors would have to eat their words. It may be a big pill to swallow for some, but I honestly think it will be necessary.

Footnote: YCharts revenue per day, avg. transaction fee/day, and total transaction fee revenue.

Disclaimers: I primarily want this post here as an “I told you so” many years down the line. I’m not counting on it taking off on forums like Hacker News, as it will likely get quickly Flagged by bitcoin stans (as happened to me before on this topic in 2021). But I also want to raise this issue now for Bitcoin’s own sake, as this issue is something the project has time to address.

[1] [On 2024’s peak day, miners received $107.76M on April 20, 2024, right before rewards were split in half, leading to an unusually high number of transactions and record TX fees, which briefly spiked to $128.45/transaction, doubling the previous record and 4x higher than at any point in the last 3 years. On that day, the network’s hash rate rose 74%. On a normal day, the TX fees are $0.50 – $4.5, with the average around $1.50]